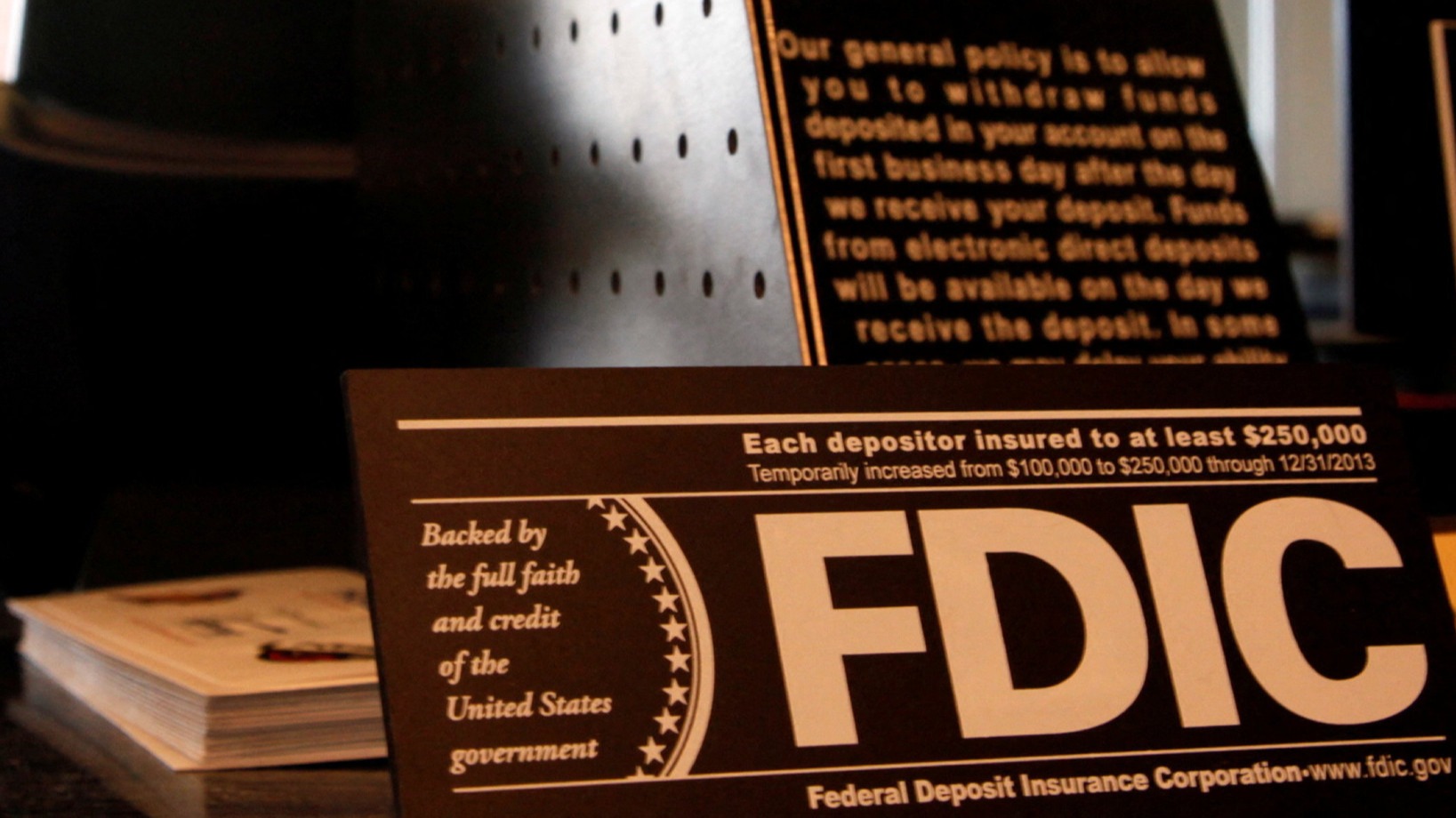

Bank failures can be distressing for both customers and the overall economy. When a bank collapses, depositors may fear losing their hard-earned money, while the stability of the financial system is put at risk. To address these concerns, the United States has established a deposit insurance fund, administered by the Federal Deposit Insurance Corporation (FDIC). This article delves into the impact of US bank failures on the deposit insurance fund, shedding light on its crucial role in safeguarding depositors’ funds.

Understanding the Deposit Insurance Fund:

The deposit insurance fund is a financial safety net designed to protect depositors in case of a bank failure. It serves as a guarantee that customers will receive their insured deposits, up to a certain limit, even if a bank goes out of business. In the United States, the FDIC is responsible for administering this fund and ensuring the stability of the banking system.

US Bank Failures and the Deposit Insurance Fund:

During times of economic uncertainty, bank failures become a concerning reality. These failures can be caused by various factors, such as mismanagement, inadequate risk management, or adverse economic conditions. When a bank fails, the deposit insurance fund steps in to protect eligible depositors, providing them with prompt access to their insured funds.

The Consequences of Bank Failures on the Deposit Insurance Fund:

Bank failures exert significant pressure on the deposit insurance fund, potentially leading to financial strain. When a bank collapses, the FDIC utilizes the funds available in the deposit insurance fund to compensate depositors for their insured deposits. In some cases, if the funds are insufficient, the FDIC may need to employ additional resources, such as borrowing from the U.S. Treasury, to fulfill its obligations.

Maintaining the Financial Stability:

The FDIC plays a crucial role in maintaining financial stability by actively monitoring and supervising banks to mitigate the risk of failures. It assesses the financial health of banks and imposes corrective actions when necessary. Additionally, the FDIC conducts regular stress tests to evaluate the resilience of banks, ensuring they have adequate capital to withstand adverse economic conditions.

The Importance of Insured Deposits:

Insured deposits provide a critical layer of protection for bank customers. The FDIC insures deposits up to $250,000 per depositor, per bank. This coverage applies to various account types, including checking accounts, savings accounts, certificates of deposit, and money market accounts. By providing this insurance, the FDIC instills confidence in the banking system and encourages individuals and businesses to deposit their funds without fear of losing them in the event of a bank failure.

Conclusion:

US bank failures can have far-reaching consequences, impacting both depositors and the stability of the financial system. The deposit insurance fund, administered by the FDIC, plays a vital role in protecting insured deposits and providing a safety net for customers. Through its supervision and monitoring efforts, the FDIC aims to maintain financial stability and mitigate the risks associated with bank failures. By understanding the importance of the deposit insurance fund, depositors can have peace of mind, knowing that their funds are protected even in uncertain times.